Copy of balance sheet form 1. Accounting statements: forms

The balance sheet is considered the main component of financial statements, and it displays all the economic activities of an enterprise for a certain time period. Thanks to a well-drafted document, you can determine whether the company’s work was successful.

At its core, the balance sheet is the main form of reporting. The document consists of several summary tables that contain information regarding the company's cash assets, debt obligations and total profits. It is worth noting that the balance sheet is compiled for a certain period of time and contains only that information that corresponds to a given period.

Dear readers! The article talks about typical ways to resolve legal issues, but each case is individual. If you want to know how solve exactly your problem- contact a consultant:

APPLICATIONS AND CALLS ARE ACCEPTED 24/7 and 7 days a week.

It's fast and FOR FREE!

The balance sheet has a prescribed form, and therefore it must be filled out with an eye to the legal requirements for this type of documentation. If a document is drawn up incorrectly and contains errors, it can negatively affect the activities of the business entity as a whole.

General points

The balance sheet is an official financial document that contains data regarding the activities of the production structure for a specified time period. This document is mandatory and must be registered with the Federal Tax Service. As a rule, most often the balance sheet analyzes data for the enterprise for the calendar year, although it is possible to draw up interim documentation for reporting periods.

The form of the balance sheet is approved at the highest legislative level, and the document consists of two subsections: assets and liabilities. The first displays all the assets that are owned and used by the company, distributed by structure and location. But the second section classifies available resources according to data on their sources.

It is worth noting that for Russian companies the balance sheet is a mandatory document, and it must be submitted to the authorized bodies to check the effectiveness of the structure. If the document was not submitted to the Federal Tax Service, then the company’s activities may be suspended.

The balance sheet, with the help of which an enterprise reports to the state on the work done, is drawn up in Form 1 or 0710001 (legally approved name of the document). Considering that the activities of various companies can be classified according to many parameters, it is permissible to use both the full and simple forms of the document.

It is quite natural that most entrepreneurs strive to act according to a more simplified scheme, and for this they use a simplified reporting form.

However, in accordance with legal requirements, this opportunity is presented only to those legal entities that meet the following criteria:

- the share of the authorized capital that is under the control of the legal entity does not exceed 25%;

- the number of hired employees does not exceed 100 people;

- the total revenue of the enterprise is within 400 thousand rubles, and does not exceed this figure.

For all other cases, you will have to fill out reports on Form 1 in full. Otherwise, this will be perceived as a violation of the current legislative framework, and the violator will be punished in accordance with the law.

Existing types

In accordance with the requirements of Federal Law No. 402 of 01/01/2013, financial statements must cover all data regarding the financial position of the analyzed business entity.

And in order to achieve this goal, the basis for preparing the balance sheet will be, and the following reporting must be included in the final document:

- annual data on the company's work;

- annual reporting for organizations whose task does not include obtaining maximum profits (non-profit structures);

- interim reporting, which is prepared for a certain period of time (3, 6 months, etc.);

- internal reporting.

If we talk about the documentation that will collectively make up the reporting, then it can be described as follows:

In turn, in addition to the traditional balance sheet, the following types of reporting documentation are distinguished:

| Balance of income and expenses | Shows the amount of cash receipts in the organization and the amount that was spent on various purposes. |

| Balance gross and net | In the first case, the document is used to improve information functions, but in the second, it allows you to determine the real value of all the company’s assets. |

| Opening balance | Compiled at the beginning of the company's work. It displays all the resources with which the organization begins to carry out its activities. |

| Final | Contains data for a previously designated period of time. |

| Liquidation balance | Evaluates the financial position of an enterprise that will soon cease to exist. |

| Working balance | The movement of funds within the company is analyzed. |

| Preliminary document | Compiled based on current performance indicators. It shows what performance results can be achieved at the end of the reporting period if current operating conditions are maintained. |

| Interim balance | Prepared before the end of the financial year. |

| Balance document | The property values of the company and the sources of their formation are characterized. |

| Consolidated | It is obtained by combining indicators for several business entities. Most often it is used by government control and statistics bodies. |

Main design nuances

The necessary conditions

Any enterprise that sets itself the task of obtaining extremely high profits uses the balance sheet as an integral part of the work process. In accordance with established legislative requirements, this form of reporting is mandatory for all structures whose work is aimed at making a profit.

Accounting statements are formed through careful analysis and control of all processes that occur in the company. In view of this, in addition to the balance sheet, it must also include other documents relating to the use of cash, the expenditure of tangible and intangible resources and the movement of capital.

In 2013, a resolution was adopted, approved by the Russian Ministry of Finance, according to which all business entities were required to submit accounting documentation to the control of authorized government agencies. At the same time, it is separately stated that those organizations that are classified as “small” businesses can submit reports in a different form, which is known as simplified.

If, at the time of approval of the resolution, the enterprise was using the simplified tax system, and until 2019 did not have time to report in the specified form, then in this case the legislator requires that all financial documents for the past several years be restored and confirmed.

After the adoption of Federal Law No. 402, reporting is submitted once per calendar year, and an explanatory note to the document is not required. After the financial year has passed, the company must submit the completed balance sheet to the tax service within 3 months. If you do not meet the specified deadline, financial measures will be taken against the company.

Formation of a liquidation account

In the event that the activity of an enterprise was considered unsatisfactory, and its owners made a unanimous decision to terminate work, then you need to know that this process is under the full control of the state. In view of this, liquidation must take place taking into account the requirements specified in Federal Law No. 129 and Art. 61-64 Civil Code of the Russian Federation.

Based on the basic rule, when completing settlement transactions with creditors, the liquidation commission, which is responsible for terminating the company’s activities, must create a liquidation balance sheet, which will display all the data on the company’s operation at the time of its closure.

This document is approved either by the body that initiated the liquidation, or by members of the company’s founding board. However, it is worth paying attention to the fact that a special form is not provided for this report, and therefore it is rational to use the form that is standard for the annual balance sheet.

The liquidation account has some features, in particular:

- The liquidation balance is automatically recognized as an inventory balance, which means that its formation occurs based on the results of the inventory and taking into account the requirements of Art. 12 Federal Law No. 129.

- The balance cannot contain leftovers, so everything possible must be done to get rid of them as soon as possible.

- When drawing up a liquidation account, the value of the property is established, which will allow us to conclude what was the main reason for the liquidation. So the valuation of a company's assets in a liquidation balance sheet will be completely different from standard reporting.

Relationship with other documents

Absolutely all forms of financial statements have close relationships with each other. When drawing up and filling out a balance sheet, it is imperative to take into account all the data on the reporting forms to determine the same results.

Thus, all indicators that in one way or another play a key role in the accounting of an enterprise should be grouped into appropriate forms. Moreover, each of them will have an independent purpose, but at the same time refer to other reports.

Often the nature of the relationship between the forms of reporting documentation is defined as logical and informational. In this case, the logical connection will be determined by the fact that the double entry rule is applied when compiling documentation. This means that the same data will be duplicated in several reports at once.

If we analyze the relationship characteristic of the balance sheet, it will have the following structure:

In addition to the fact that close connections are available in the main forms of reporting, relationships will also be established between individual balance sheet items. This will be expressed in the fact that some lines of the document will be defined as adding or subtracting other lines.

Sample of filling out a balance sheet:

Example of filling out a balance sheet form

The approved balance sheet form for 2019 must be completed in such a way as to comply with all legal requirements. This operation begins by filling out the required details. After which you can proceed to displaying all the necessary indicators on the financial activities of the business entity.

With all this, it is important to pay attention to the basic rules:

- Data at the beginning of the reporting period must be displayed in the document and correspond to the information that was available at the end of the previous period.

- The results for the “asset” and “liability” subsections must be completely identical.

- All information must be presented in detailed form. The presence of offsets between balance sheet items is not permitted under any circumstances.

- All data presented in the balance sheet must have appropriate documentary evidence.

The reporting document will consist of many separate lines, the main ones of which will be:

At the end of the document, a total is compiled, which must be equal for all subsections. This means that the total value of assets and liabilities should be identical and not different.

In order to better understand how the document is filled out, you need to download the form for free on specialized Internet sites dedicated to accounting issues and study a sample of filling out Word (Word).

Other requirements

With regard to the rules for drawing up a balance sheet, the legislator puts forward quite strict requirements, which must be taken into account and displayed in the final document.

In particular, the document must have certain details:

- OKUD classifier and type of activity of the company according to;

- the exact date on which the report was compiled (as a rule, this is the first day of the coming month or the last day of the current one);

- information on the organization, namely the full name of the structure, TIN, organizational form, form of ownership, exact location (it is important that all data presented correspond to the information specified in the constituent documentation);

- date of acceptance and approval of the document, as well as a mark on the date of sending the balance for accounting to the tax service;

- specific unit of measurement (thousand or million rubles).

Balance sheet (form No. 1). Instructions, rules and filling procedure

Balance sheet- this is a way of generalizing and grouping the assets of the economy and the sources of their formation - liabilities - at a certain date in monetary value. Balance sheet indicators characterize the financial position of the organization as of the reporting date.

The main task balance sheet– show the owner what he owns or what capital is under his control. The balance sheet allows you to get an idea of material assets, the amount of reserves, the state of payments, and investments. Balance sheet data is widely used for subsequent analysis by the organization's management, tax authorities, banks, suppliers and other creditors.

Consists of 2 main parts - asset And passive. The asset represents the organization's resources, and the liability represents the sources of their formation. A distinctive feature of the balance sheet is the equality of the totals of assets and liabilities. This is due to the double entry principle used in accounting.

Assets The balance sheet contains 2 sections:

- I. Non-current assets;

- II. Current assets.

Passive The balance sheet consists of 3 sections:

- III. Capital and reserves;

- IV. Long term duties;

- V. Short-term liabilities.

Each asset and liability element of the balance sheet is called balance sheet item. Asset items reveal the nature of resources, their use and magnitude. Liability items characterize the sources of resource formation, namely: from what source this part of the assets was created, for what purpose they are intended and their value.

When preparing a balance sheet, keep the following in mind:

- the balance sheet data at the beginning of the year must correspond to the data at the end of last year (taking into account the reorganization);

- offset between items of assets and liabilities, items of profit and loss is not allowed, except in cases where such offset is provided for by the relevant Accounting Regulations;

- the corresponding balance sheet items must be confirmed by inventory data of property, liabilities and settlements.

The standard form of the balance sheet is regulated by the Ministry of Finance (). However, organizations can independently develop a balance sheet form, using the standard one as a template. In this case, the general requirements for accounting reporting must be observed.

When developing and adopting the balance sheet form (Form No. 1), it is recommended to use the total line codes and line codes of sections and groups of items given in the sample balance sheet form. If a transcript is provided for any indicator in a balance sheet developed by an organization independently, then the articles in this transcript are coded by the organization itself.

The balance sheet contains the following required details:

- the reporting date as of which the balance sheet is presented;

- full name of the organization in accordance with the constituent documents;

- taxpayer identification number (TIN);

- the main type of activity of the enterprise with the OKVED code;

- organizational and legal form/form of ownership (according to the OKOPF and OKFS classifiers);

- unit of measurement - thousand rubles. (OKEY code 384) or million rubles. (OKEY code 385);

- location (address);

- date of approval (indicates the established date for the annual financial statements);

- date of sending/acceptance (the specific date of postal, electronic and other sending of financial statements or the date of their actual transfer according to ownership is indicated).

Total figures for balance sheet items are given in thousands of rubles without decimal places. Organizations with significant sales turnover, liabilities, etc. can provide data in millions of rubles (without decimal places).

Indicators about certain types of assets, liabilities, income, expenses and business transactions can be presented in the balance sheet in a total amount with disclosure in , if each of these indicators individually is not significant for the assessment by interested users of the financial position of the organization or the financial results of its activities.

Let's consider procedure for filling out Form 1 "Balance Sheet".

- accounted for in off-balance sheet accounts

In the column " At the beginning of the reporting year" shows data at the beginning of the year (opening balance sheet), which must correspond to the data in the column "At the end of the reporting period" of the previous year (closing balance sheet), taking into account the reorganization carried out at the beginning of the reporting year, as well as changes in the assessment of financial reporting indicators associated with the application of the Regulations on accounting and financial reporting in the Russian Federation and the Accounting Regulations “Accounting Policy of the Organization” PBU 1/98.

In the column " At the end of the reporting period" shows data on the value of assets, capital, reserves and liabilities at the end of the reporting period (month, quarter, year).

All legal entities are required to submit financial statements, and this documentation is submitted both to the tax authority and to the statistical authority. The reporting must include specialized forms of documents 1 and 2, as well as a report on all changes that occur with capital, and a specialized report on cash flows in the enterprise. A prerequisite is the preparation of an auditor's report, which reflects the reliability of all accounting reports.

It should be noted that individual entrepreneurs do not submit such reports, and certain entrepreneurs who are classified as small businesses can use a simplified version of reporting. Only financial results of indicators are presented in a simplified form. In fact, the document is drawn up without certain details. There are also applications that provide more advanced data. These applications are filled with the most significant indicators, without which it will be impossible to carry out analytical actions on the operation of the enterprise.

Any business activity requires the formation of various reports, on the basis of which the process of analyzing the internal state of the enterprise is carried out, and government agencies have the opportunity to assess the correctness of tax calculations, etc. The correctness of the preparation of these documents depends on a detailed study of all the nuances of the preparation structure. Successful business also depends on the results obtained, a correctly conducted analysis, on the basis of which the company has the opportunity to correctly distribute funds for more intensive development of its activities.

In clause 5, part 1, art. 23 of the tax legislation determines that all types of reports must be submitted in two versions, and the reporting period is set at one year. If an enterprise prepares and calculates interim reports, then they can also be submitted to the tax authority and the statistics department. In this article we will talk about how financial statements are prepared according to established forms, taking into account all the nuances, and we will reveal the essence of the correct preparation of all mandatory document lines.

Balance- the most significant document that actually characterizes all the features of the organization’s activities over a clearly defined period of time. Based on the balance sheet, you can determine the current position of the enterprise.

This balance sheet provides a kind of separation of assets and liabilities. Moreover, the division is carried out depending on the maturity date or circulation on the basis of the periods for which certain obligations or assets were issued. The division is carried out into the short-term (short period of time) and long-term perspective. All assets, as well as liabilities, are considered short-term if the duration of the operating cycle does not exceed a year. If the period is more than a year, then in this case a long-term perspective or obligation is formed.

All data that is entered into this balance sheet is capable of revealing the nuances of the development of the enterprise; the organization’s specialists, based on the balance sheet, carry out an analysis of activities; it must also be said that this version of the reporting is submitted to the tax authority and the statistical department.

The legislator establishes a clearly developed form of the document, which was adopted by Order of the Ministry of Finance of Russia dated July 2, 2010 No. 66n. At the same time, it is established that when drawing up a balance sheet, the organization has the right to independently determine all indicators, taking into account the importance of certain parameters.

The balance sheet in Form 1 contains two main parts:

- Assets;

- Passive;

The asset section provides data on all resources that the organization has. The next section provides information on the issue of creation and emergence of assets. The peculiarity of this balance sheet is that a kind of equality of totals for liabilities and assets is formed. This structure is due to the fact that the principle of double entry has been formed.

Compilation instructions:

- The first asset block contains two sections. Data on non-current and current assets is indicated here. The residual parameters of the value of these assets should be entered on line 1110. At the same time, it is this parameter that allows you to analyze the activities of the enterprise, allows you to determine that the object has the ability to bring economic benefits in the future, or is already bringing this benefit, and the object is aimed at long-term prospects for your work. As for current assets, in this case we are talking about recording data on the cost of inventories. The data is reflected in line 1210. This includes the cost of raw materials, as well as materials, all costs that determine work in progress. The cost of goods and products that are actually purchased and are in stock, etc. is indicated;

- The passive has three sections. Each section includes the need for a detailed description of the data. Capital and reserves - a section that includes all data relating to authorized capital, as well as the shares of investors. Long-term liabilities are a reflection of all borrowed funds and credit obligations. In fact, this section reflects information that can reveal the negative balance of the enterprise, taking into account the long-term perspective. Short-term liabilities are an indication of the amounts of borrowed or credit funds that will be repaid within a year.

All elements of liabilities and assets are considered balance sheet items. All asset items are capable of revealing the essence of those resources that are available to the enterprise and can be used as an element of development; the amount of assets is also determined. Liability items are capable of revealing all data on the sources of resource formation. In fact, data on borrowed and credit funds is determined, which makes it possible to determine the effectiveness of such actions and the prospects for the development of the enterprise.

- All data that is reflected in the accounting type balance sheet must necessarily correspond to the data that was recorded in other balance sheets at the end of the reporting period (end of the year). In case of reorganization, this fact is taken into account;

- The formation of offsets between items of liabilities and assets, between losses and profits is not allowed. At the same time, the legislator provides for the possibility of such offset; however, an additional application will be required;

- All items on assets must actually be confirmed by documents reflecting the inventory, calculations, obligations, etc.

The standard form of the document is approved by law. However, it must be taken into account that the information entered into the document is determined by the management of the enterprise, taking into account its significance. For example, minimum loan obligations for a short period may not be reflected in the reporting documents. But when it comes to a loan that is issued for several years, such data must certainly be reflected in the report.

An enterprise has the right to base it on Form 1, but create its own form. However, you need to be guided by the general rules and requirements for preparing accounting-type reports.

It has been established that the following mandatory details must be indicated in the balance sheet:

- The date when the balance sheet process is carried out and the date of the reporting period for which this reporting documentation is compiled and provided is determined;

- The need to indicate the full name of the organization is established, and the legislator requires that the specified name correspond to the data specified in the statutory documents;

- You also need to indicate the tax payer number, as well as the main activity codes of the enterprise. It is necessary to indicate the classification of OKOPF and OKFS. The units of measurement that are used in the process of drawing up the document are indicated, and the legal address of the enterprise is also provided;

- The date the document was actually sent to the appropriate authorities.

All total parameters of balance sheet items must be provided in thousands of rubles; accordingly, decimal places are not indicated. If the company has a more significant turnover, then the data can be provided in millions. All amounts of certain assets may be presented as a total amount, subject to disclosure in the notes accompanying the balance sheet. But such actions are carried out if the indicators are not important and can be generalized.

First section: Non-current assets:

- These are certain works of science, programs, inventions, models, production secrets, and even business reputation. This includes all research expenses, which are reflected in account 04, and are indicated on line 1120 in the balance sheet. Search assets are also indicated. These indicators should be reflected in lines 1130 and 1140;

- Fixed assets must be indicated in line 1150. In fact, the line reflects information about fixed assets as the initial cost. These funds also include property received by the enterprise under a leasing agreement, as well as all objects that are required to undergo state registration of ownership;

- A description of information about investments of a financial type is generated. A division is established into short-term investment options, if the period is no more than a year, as well as longer-term investments. To indicate the amounts of long-term investments, line 1170 is provided. All investments made in subsidiaries, acquisition of shares, etc. are also reflected here;

- There is a section - long-term assets, which are reflected in line 1190; data is generated if you need to reflect long-term loans with a term exceeding one year. There are also short-term investments that are posted on line 1230;

- Deferred assets are indicated in line 1180, and the simplifiers do not fill out this line, but do not put a dash, but simply leave it blank. Line 1190 indicates data that relates to all other non-current assets.

Second section: current assets:

- First of all, data on working inventories is indicated. An indication of the cost of all material inventories that the enterprise has is generated. The data is reflected in line 1210. The indicator does not need to be decrypted. But, if the inclusions in line 1210 are important, for example, the division into the costs of work in progress and the costs of raw materials, then in this case there is a need to decrypt the data;

- VAT is indicated, the data is indicated in line 1220. Simplified people do not fill out this line, since they reflect input VAT on accounts 19, and in fact, under this taxation system, VAT is not paid;

- Line 1230 defines accounts receivable data. The line contains information about short-term debt obligations. Investments of the financial type are reflected in line 1240. The indicator determines those types of funds that were provided as a loan for a year (no more);

- A line with indicators of cash equivalents and cash is filled in. To fill out these lines, you will actually need to sum up all cash equivalents - account balances, cash in accounts 50, 55, 52, 57. In line 1260 you can indicate all other current assets that could not be entered in another column of the document.

Third section: Capital and reserves:

- The details of the authorized capital are indicated in line 1310. The amount indicated in this line must clearly coincide with the data set forth in the statutory documents;

- It is mandatory to indicate data that reflects the presence of own shares, which were acquired by the organization from shareholders in the course of its activities. Such data is entered in line 1320. In the case when own shares were bought back and then resold, they are considered an asset. This means that their data must be entered in line 1260;

- All other current assets are entered in line 1340. This shows the actual revaluation of all objects and those intangible assets that are held in the additional capital account;

- Additional capital without revaluation is reflected in line 1350. The indicator for this line is reflected only without the amount of revaluation. This is followed by a line with reserve capital, their balance is reflected in line 1360. Deciphering all data on reserve capital is required when some data is essential, very important for analyzing the operation of the enterprise;

- The values of the uncovered loss must be indicated. All undistributed profit options must be reflected in line 1370. Data on the amount of uncovered loss is also entered here. This amount is reflected in brackets. Certain indicators of this loss or retained earnings can be deciphered in additional lines. In fact, it is possible to provide a more accurate financial result for profit and loss.

Section Four: Long-Term Plan Commitments

An indication of borrowed funds is immediately generated. Line 1410 is filled in, in which data on the enterprise’s debt for all long-term operations is entered. In fact, this reflects the data of credit and loan obligations, taking into account the fact that their fulfillment will be carried out for more than one year. Tax payers on profits received are required to compile line 1420;

All estimated liabilities are reflected in line 1430; it should also be noted that contingent liabilities and assets are not always reflected in the document, since the organization may not recognize these indicators in accounting;

All other liabilities are reflected in line 1450.

Fifth section: short-term liabilities

- All funds that were received by the organization for a short period of time are reflected in line 1510;

- The total amount of credit debt should be reflected in line 1520. If the amount of debt is significant, then it should not be generalized, but described taking into account significant credit obligations;

- Line 1530 is filled in if your company receives certain budget funds or amounts for targeted financing;

- Provisions are reported on line 1540, but only if the company recognizes this use of the liability.

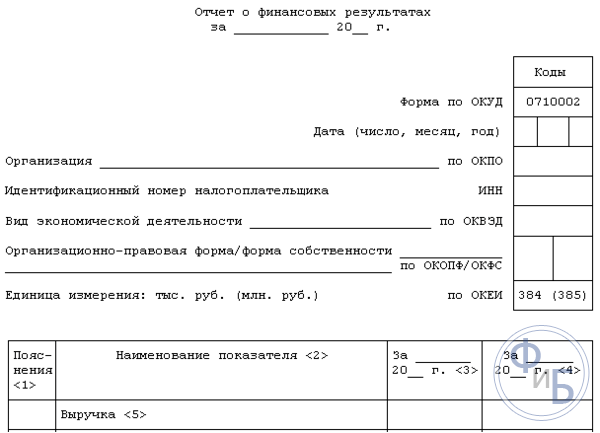

This is a reporting form that contains information about expenses, income and financial results. The form is approved by law and contains information about all the organization’s actions. By drawing up this document, you can determine the rationality of the organization’s activities, calculate profits, etc.

The form of this document establishes the need to provide the following information:

- Indication of the period for which data is provided, as well as dates, provision of information about the organization, as well as indication of units of measurement;

- The following is a table with reporting indicators. This is the number of explanations, indicator data and specialized codes, as well as a column with the value of indicators for a clearly defined reporting period of time. And the same column with the indicators that were provided last year.

How is Form 2 compiled?

- Revenue data is indicated in line 2110. It is necessary to show all income data that relates to the usual activities of the enterprise.

- In line 2120 you will need to indicate the cost of sales. In fact, the amount of expenses for all types of activities of the enterprise is indicated. For example, expenses that are formed on the basis of production of products, purchase of raw materials, performance of certain works;

- In line 2100 you will need to indicate the gross result. This is ordinary profit data excluding all administrative and selling expenses. To calculate this indicator, you need to deduct the cost of sales from the amount of revenue. If a negative indicator is formed, it is indicated in brackets (round brackets are used);

- All commercial expenses that are generated at the enterprise are entered in line 2210, and administrative expenses are indicated in line 2220;

- Line 2200 contains an indication of data in the form of profit or loss of the enterprise. The calculation is carried out by deducting commercial and administrative expenses from the amount of gross profit;

- All income that is received indirectly is reflected in line 2310, for example, indicating dividends or the value of property. Income received from participation in other organizations is indicated in line 2310, and the interest that the enterprise receives on loans and securities is indicated in line 2320;

- The interest that the company will pay itself is indicated in line 2330, and other expenses in the next two lines;

- Line 2300 indicates tax profit. This line shows the accounting profit or loss from the activities of the enterprise, but the current tax indicators should be reflected in line 2410.

Net profit should be reflected in line 2400. After compiling this table, reference information is provided. The results of the revaluation of non-current assets are indicated, without taking into account net profit. It is imperative to indicate the results of all transactions that did not include net profit. Data on the overall financial result, etc. is provided.

This form must be signed by the supervisor. Previously, the document was necessarily signed by the chief accountant; today, the document should not contain this detail, but at the same time, the legislator does not prohibit the accountant’s signature on the document.

conclusions

The need for entrepreneurs and legal entities is the preparation of specialized accounting-type documentation. Individual entrepreneurs do not have to draw up certain documents, and the system for providing balance sheets for enterprises operating in small businesses has also been simplified. Drawing up forms 1 and 2 has a lot of nuances. However, the legislator clearly developed the document forms and provided instructions, based on which the process of filling out documentation becomes simpler and faster.

Completing Form 2 is a simple process. The form is presented in the form of a table, where you simply need to enter certain data about the activities of the enterprise. As for Form 1, the structure of its preparation will be more complex, since a lot of different data needs to be indicated there, for verification by the tax structure, as well as for the statistical department. Forms of documents that must be submitted in accordance with the law can be found on the official website of the Federal Tax Service. This is where you can find up-to-date forms that need to be filled out at the current moment in time.

You can also watch a lot of videos on the Internet on the issue of preparing balance sheets; here is a video that will certainly help you in this matter.

Balance sheet form No. 1 - sample filling, form, which is filled out in thousands of rubles, or millions, and does not contain decimal places. If there is foreign currency, then it is converted into domestic currency based on the Central Bank exchange rate as of December 31.

The balance sheet and all its items are filled out on the basis of data that is reflected in the balance sheet.

Balance sheet is of some interest not only to the tax authority, but also to state statistics; in addition, it is of interest to the enterprise itself, in particular to the management of this enterprise, and employees of the analytical department. According to the data contained in the balance sheet (the amount of capital, reserves, financial investments, reserves, debt), long-term as well as short-term financial and economic planning is carried out.

Balance sheet form No. 1 – structure

The balance sheet has two sections: liabilities and assets. An asset contains information about the resources that an enterprise has at its disposal. These resources are divided into two groups, which represent two parts of assets, these are non-current assets of the balance sheet, non-current assets.

The balance sheet liability allows for an idea of the sources of formation of the enterprise's resources. The liability includes three sections:

Long term duties;

Capital, reserves;

Short-term liabilities.Rules for drawing up a balance sheet

The standard form was approved by the Ministry of Finance on July 2, 2010, by order No. 66n. To this order, an edition was issued under number 124n, dated 10/05/2011.

The legislation allows enterprises to independently develop a convenient form of balance sheet for themselves, while retaining sections that make it possible to fully disclose all information regarding the financial condition of the enterprise. The codes for line items, balance sheet sections, and total lines must necessarily match all the codes provided for in the standard form.

When drawing up a balance sheet, an enterprise accountant adheres to the rules, which should include:

All data obtained at the beginning of the year must be reflected in the balance sheet, and fully correspond to all data that was at the end of the previous period.

The totals of assets and liabilities must be equal.

All data must be provided in expanded form; offsets between liability and asset items are not allowed.

The information contained in the balance sheet items must have appropriate confirmation, be it documents regarding the formation of reserves, reconciliation reports, or inventory sheets for the enterprise.Balance sheet - filling process

The top line indicates the reporting lady for whom the balance sheet was drawn up. After this, you must indicate the full or abbreviated name of the enterprise (according to the statutory documents), the taxpayer’s INN, and the main type of activity (as approved by the statistical authorities).

After this, you need to register the code of the legal form of the enterprise, OKOPF and OKFS, select a convenient unit of measurement, after which you need to indicate its code. The line “Location (address)” must correspond to the legal address of the enterprise.

The line “Approval date” corresponds to the date for annual reporting. Next, in the line “Date of sending/acceptance” you must enter the date of sending the statements, or the actual date of transfer of the balance.

The balance (form No. 1) must be confirmed by the signature of the chief accountant and the manager with a full transcript. The date is indicated at the bottom of the title page, also opposite “Date”, the year, month, and day are indicated.

The completed balance sheet form No. 1 is a sample of completion; in some cases the form must be submitted to the tax authorities.

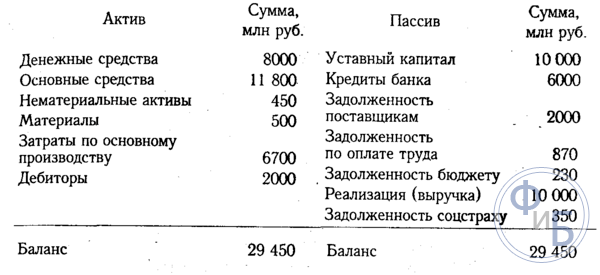

You can see a sample of Forms 1 and 2 of financial statements in our material. We will tell you about the purpose of these forms and show you with an example how to calculate net profit according to the indicators of Form 2 and where to reflect the result of these calculations in Form 1.

Form 1 and Form 2 of financial statements

Forms 1 and 2 of financial statements are the main reporting forms - these are the balance sheet and the income statement. Not a single set of reporting documentation for any company can do without them.

- A balance sheet is a set of indicators of a company’s performance as of the reporting date (about the residual value of fixed assets, cash balances in accounts and on hand, accounts payable and receivable, etc.);

- Income statement- this is data on revenue, expenses and profit for the reporting period of time.

These forms are supplemented by other related reports (capital flow, cash flow, etc.). The information contained in them explains and details the data reflected in Form 1 and Form 2 of financial statements.

Forms 1 and 2 are present in accounting reports compiled for any period (month, quarter, year). For example, the minimum set of financial statements for the 1st quarter of 2018 (if the company prepares interim accounting statements by decision of the owners or for other reasons) must necessarily include both forms. At the same time, such a reporting set can be supplemented with detailed explanations (if there is a need for them).Both reports have a unified form approved by order of the Ministry of Finance of the Russian Federation dated July 2, 2010 No. 66n.

Form 1: balance sheet

The balance is a table divided into 2 parts:

- Part 1. A balance sheet asset is the property and liabilities of a company used in its activities and capable of bringing benefits to it in the future.

- Part 2. Balance sheet liability - reflects the sources of formation of the balance sheet asset.

In a correctly drawn up balance sheet, the equality is satisfied:

balance sheet asset items = balance sheet liability items

In more detail, this equality for Form 1 of the financial statements looks like this:

Section 1 + Section 2 = Section 3 + Section 4 + Section 5,

- Section 1 - the cost of non-current assets (long-term used property, the cost of which is repaid in installments).

- Section 2 - the cost of current assets (quickly turnover and quickly redeemed assets: materials, inventories, etc.).

- Section 3 - the value of capital and reserves (sources of the company's own funds).

- Section 4 and Section 5 are long-term and short-term liabilities expressed in monetary terms, respectively (the company's obligations to pay loans, loans, taxes, wages, etc.).

Using the balance sheet (Form 1 of financial statements) you can:

- analyze and evaluate the financial condition of the company as of a specific date;

- track the dynamics of changes in indicators over time (comparing indicators of balance sheets compiled as of previous reporting dates);

- conduct an economic analysis of the company’s activities and, on its basis, make informed management decisions.

Form 2: Statement of financial results

The financial results report (Form 2) presents a table containing the company's performance indicators for the reporting period. They allow you to calculate a number of important financial indicators (gross profit, profit before tax, net profit, etc.).

A special feature of Form 2 is the relationship between all rows of the main table. It helps to assess the impact of a company's income and expenses on the final financial result (net profit).

All indicators are given for the reporting period of the current year and the same period last year. This allows you to track the dynamics of changes in indicators included in the financial results report.

Let's look at an example of how a company's net profit is calculated based on Form 2 indicators.

Example

The revenue of Park House LLC for the 1st quarter of 2018 amounted to RUB 3,456,128. (excluding VAT and excise taxes) with the cost of services being 1,377,809 rubles, management expenses - 544,322 rubles.

Using these numbers from Form 2, we calculate 2 indicators:

- Gross profit = Revenue - Cost = RUB 3,456,128. - RUB 1,377,809 = 2,078,319 rub.

- Sales profit = Gross profit - Administrative expenses = RUB 2,078,319. - 544,322 rub. = 1,533,997 rub.

Park House LLC received a loan in 2018, the interest accrued for the 1st quarter amounted to 230,000 rubles. Other income and expenses amounted to RUB 998,343, respectively. and 1,466,321 rubles.

Using these numbers, we calculate the following indicators of Form 2:

- Profit before tax = Profit from sales - Interest payable + Other income - Other expenses = RUB 1,533,997. - 230,000 rub. + 998,343 rub. - RUB 1,466,321 = 836,019 rub.;

- Current income tax = RUB 836,019. x 20% = 167,204 rubles;

To calculate net profit, you also need the amounts of changes in IT and ONA (deferred tax assets and liabilities) for the reporting period. According to the accounting data of Park House LLC, they amounted to 339,123 rubles. and 38,763 rubles. respectively.

Let's determine the net profit of Park House LLC:

Net profit = Profit before tax - Current income tax - IT + SHE = 836,019 rubles. - 167,204 rub. - 339,123 rub. + 38,763 rub. = 368,455 rub.

The result of the calculations falls into the line “Retained earnings (uncovered loss)” of Section 3 of Form 1.

What a sample accounting report looks like - forms 1 and 2 - see below.