What is the total cost of a loan (FCC)

What is the total cost of a loan? Why is this indicator needed? What costs are included in the calculation? Is it possible to calculate the UCS value on my own and how to do it correctly? Why in most cases the calculation will be wrong? These and many other questions are answered in this article.

If the name of the organization (for example, an appraisal office) is written in the contract, then the calculation will be made according to the tariffs of this organization.

It happens that the contract provides for several third parties. For example, insurers with a choice. Then the calculation will be based on the tariffs of one of them.

If the range of insurers is not limited to the bank, then the tariffs of ANY insurance organization known at the time of calculation are used.

That is, the value of the indicator written in the contract will be approximate!

Important! The bank must disclose information about the insurance company, according to the tariffs of which the calculation is made. The bank is also obliged to indicate that when drawing up an agreement with another insurer, the value of the TIC will be different.

When accounting for insurance premiums in the TIC indicator, inaccuracy may also be associated with other features of the calculation.

The law allows (clause 5, article 4 in the comments of the Consultant) to calculate the cost of third-party services at the company's rates without taking into account the personal characteristics of the borrower.

For example, for auto insurance without taking into account the age or driving experience and features of the car (performance, brand, year of manufacture).

Then the bank is obliged to notify the borrower about this.

When determining the value of PSK, the tariffs in force at the time of calculation are used. They may change in the future. Then the PSK in the contract will differ from the actual one.

6 The price of insurance, when NOT the borrower and NOT his relative receive compensation for the insured event.

For example, the PIC will include life and health insurance for the amount of the loan, if, upon the occurrence of an insured event, it will be received not by the borrower, but by the bank to repay the loan.

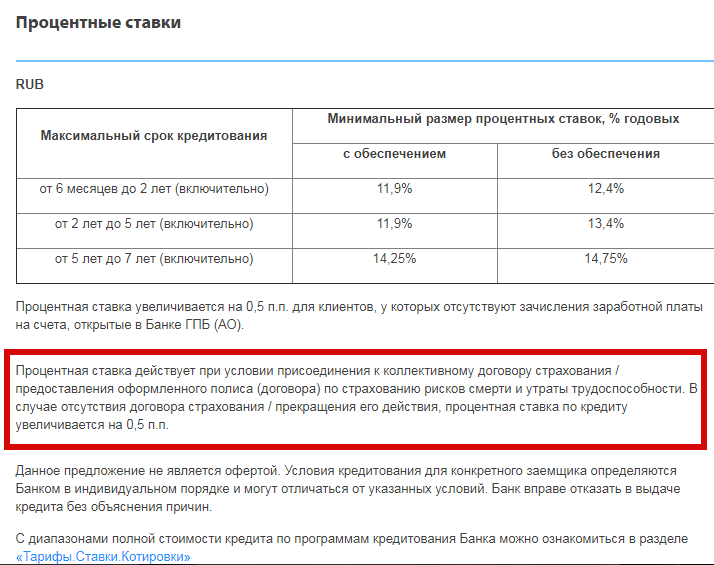

7 Insurance, if it specifies the terms of the loan. Including terms, rates and amounts.

For example, Gazprombank on consumer loans indicates that the interest rate increases by 0.5 percentage points if there is no insurance contract or its validity is terminated. The bank is obliged to take into account this insurance.

Click to enlarge image

What does the bank not take into account when calculating TIC?

1 Payments are required by law.

For example, OSAGO is not taken into account in the calculation.

2 Payments in case of breach of contract by the borrower.

For example, penalty for late payment. Moreover, it is impossible to determine in advance whether the borrower will pay on time or late.

3 Payments dependent on the decisions of the borrower. They must be related to the loan and stipulated by the contract.

For example, cashout fee or early payment fee.

4 The price of collateral insurance, for example, CASCO.

5 Insurances with conditions:

- registration of insurance does not affect the credit decision of the bank and the price of the loan;

- the borrower receives additional benefits from these services (for example, with a car loan, the rate for life insurance is different from such a rate without a loan);

- within 14 days, the borrower can refuse these services.

For example: if the borrower's life and health insurance for a car loan meets these conditions, the bank MAY not add insurance to the calculation.

Important. These exceptions allow banks to vary the terms of loans so as not to take into account insurance.

What is really going on? What do Sberbank and Alfabank take into account in the PSK?

The law provides general provisions and does not give instructions on the inclusion in the calculation of each specific insurance or other additional payment. This gives rise to various interpretations and allows creditors to consider how it is more profitable for them.

The law provides for many exceptions, which also plays into the hands of bankers.

In addition, bankers sometimes do not know how to correctly interpret the article of the law. This is evidenced by requests to the Central Bank from their side asking for clarification.

Click on the picture to enlarge

If the actions of the bank are legal, but not all payments are taken into account in the calculation, there is no point in complaining and writing applications. It is important to understand that your loan is associated with certain expenses. They may not be included in the calculation of the cost, but they will be provided for by the contract - read it carefully.

Make an independent calculation, taking into account all possible payments. Then there will be no surprises and you will be able to competently manage your own money, planning future expenses.

PSK calculates the bank and the borrower on their own.

The bank makes a calculation and notifies the borrower:

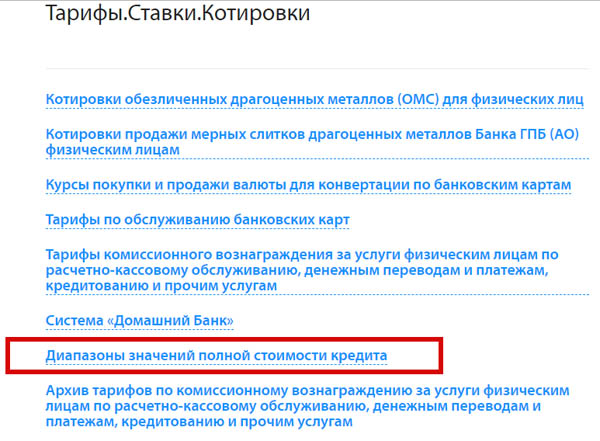

1 When placing loan offers on the official website. The bank is obliged to disclose information about the terms of the loan. The range of UCS is indicated for each product. This method should be used at the stage of analysis and selection of loan offers.

True, in some cases, you have to look for this information on the site.

For example, Gazprombank, describing the terms of loans, at the very end gives a link to the section "Tariffs. Rates. Quotes", where you can find the range of TIC. But here, too, you first need to select a specific section, then open the file in the "pdf" format.

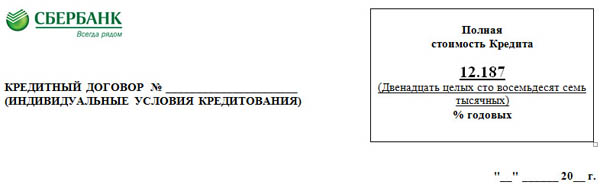

2 When drawing up a loan agreement. Or when conditions change on it. Here you can see the TPS at the time of the contract. You can check with your calculations taken from the first paragraph.

The value of the UCS is indicated on the first page of the contract in the upper right corner in a square frame. The indicator is printed in capital letters in large black type.

3 In case of early repayment of part of the debt.

How to calculate the total cost of the loan yourself?

Why calculate the PSK yourself?

- you need to get the exact value before signing the contract.

The bank's website indicates the range of TIC values, since the rate and other loan conditions differ for different borrowers;

- if you need to compare different loan options;

- if there is no trust in the bank, which does not take everything into account in the calculation. For example, Alfabank takes into account the cost of assessing collateral for a mortgage, Sberbank does not.

The calculation of the full cost is different from the calculation of the interest rate on a loan. The calculation formula is given in article 6 of the law.

Click to enlarge image

The formula is complex, and not always even a banking specialist understands the meaning and procedure for its calculation. Let's look into it.

The total cost of the loan corresponds to the internal rate of return. In financial mathematics, it is denoted by IRR (English internal rate of return).

The value corresponds to the interest rate at which the net present value (NPV) is zero.

What is net present value? First, let's define what income, expenses and net income are.

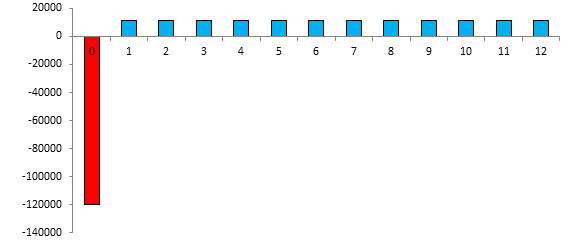

Let's illustrate the cash flows on a loan in the amount of 120,000 rubles, for a period of 12 months at a rate of 28%.

Provided that the payment is annuity (all payments to repay the loan have the same amount), the value of each payment will be 11,581.72 rubles. These payments are shown in blue and are loan income. Income from the point of view of the bank that will receive these amounts.

The red color shows the loan expense for the bank - this is the loan amount itself 120,000 rubles.

| payment date | payment number | payment type | amount, rub. |

| 10.Jan.18 | 0 | consumption | -120000 |

| Feb 10, 18 | 1 | income | 11580,72 |

| 10.mar.18 | 2 | income | 11580,72 |

| 10.apr.18 | 3 | income | 11580,72 |

| May 10, 18 | 4 | income | 11580,72 |

| 10.jun.18 | 5 | income | 11580,72 |

| 10.Jul.18 | 6 | income | 11580,72 |

| 10.Aug.18 | 7 | income | 11580,72 |

| 10.Sep.18 | 8 | income | 11580,72 |

| 10.oct.18 | 9 | income | 11580,72 |

| 10.Nov.18 | 10 | income | 11580,72 |

| 10.dec.18 | 11 | income | 11580,72 |

| 10.Jan.19 | 12 | income | 11580,72 |

| Total | 18968,64 | ||

The bank's net income (overpayment to the client) is the difference between all income and expenses. In our case, it turned out to be 18,968.68 - highlighted in bold in the table.

Now let's look at net present value. All loan payments are made at different times (dates are indicated in the table). Date of issue is red. All the rest - blue - payments with an interval of 1 month.

Money loses its value over time. Today I will buy a large chocolate bar for 100 rubles, and in a year it will cost 120 rubles. That is, in a year, 100 rubles will not be enough to buy a chocolate bar. So 100 rubles. different amounts today and next year. In our example, 100 rubles. today correspond to 120 rubles in a year.

Discounting is the reduction of future money to today's value. That is, if we bring to the present moment (discount) the cost of a chocolate bar next year (120 rubles), then we get 100 rubles.

All loan payments must be discounted to the loan disbursement date. Net present value is the sum of all discounted payments.

We need to determine the discount rate at which the net present value will be zero. That is, today's 100 rubles. will be equal to 120 rubles in a year. This IRR rate. It will correspond to the value of the total cost of the loan.

In the loan example, this is the rate at which the overpayment would be zero. That is, a loan of 120,000 rubles. will be equal to the sum of all discounted payments of the client in favor of the bank.

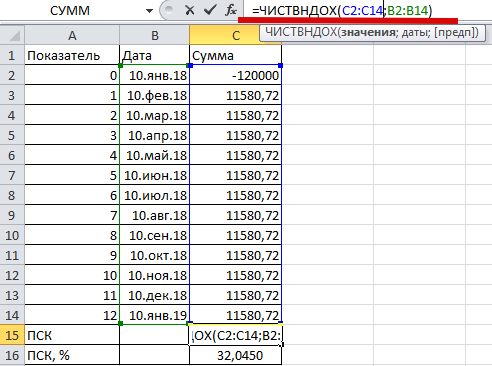

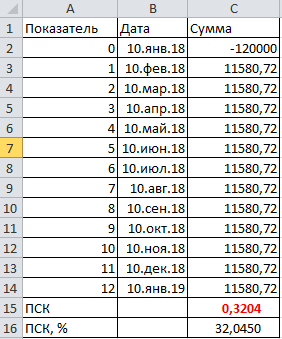

For self-calculation, you will need the EXEL program.

Dates are entered in column "B". The first date (or rather, zero) is January 10, 2018 - the date of loan approval. On this date, we make a calculation (discount) and determine the IRR or the total cost of the loan.

In column "C" indicate the amount. The first amount is negative - approved loan. The rest are positive - all payments are on schedule.

EXEL has a built-in function for determining IRR (in our case, UCS), it is called "CHISTVNDOH".

To calculate, in the cell "C15" we enter the equal sign and the name of the formula "CHISTVNDOH". In the figure, the formula is shown in the formula bar, underlined in red.

Then, in brackets, we first enter all the values (blue font in the formula and blue range in the table), then dates (green font in the formula and green range in the table).

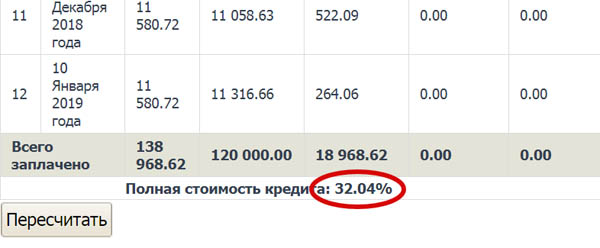

We press "enter" and see in the cell "C15" the value 0.3204 (bottom figure). This is the full cost of the loan. Only it is expressed, not as a percentage, but in fractions of a unit. To express as a percentage, we multiply the value by 100. The result is visible in cell "C16". It turned out 32.04.

So, with a loan for a period of 12 months, in the amount of 120 thousand at a rate of 28% per annum, which corresponds to a monthly payment of 11,580.72 rubles, the TIC will be 32.04.

Important. In this example, loan payments are considered as input data. How and where can a borrower get them?

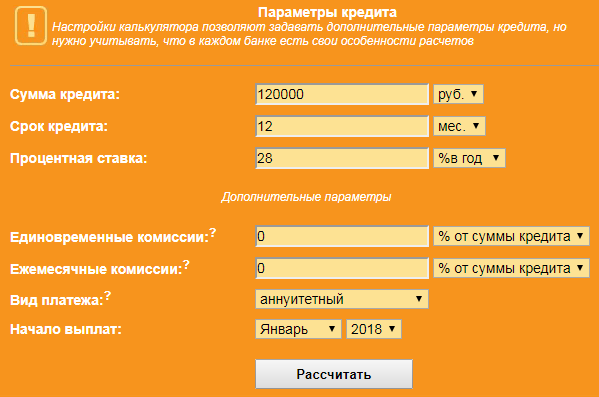

In the loan agreement in the payment schedule. If there is no agreement yet. You need to make your own payments. To do this, you can use any online loan calculator.

We enter all known parameters of the loan into the form, click "Calculate" and see the result. The amount of the monthly payment in the figure is circled in red.

Choose a calculator to calculate the PSC. For example, this one: www.ipotek.ru/calc2n/results.php?matr=4

Specify the loan parameters (take the previous example):

- a period of 12 months;

- amount 120,000;

- rate 28;

- approval date January 10, 2018

If necessary, we enter information about insurance and other additional payments in the form. While we will consider without insurance.

We get 32.04%, which corresponds to the value calculated in EXEL.

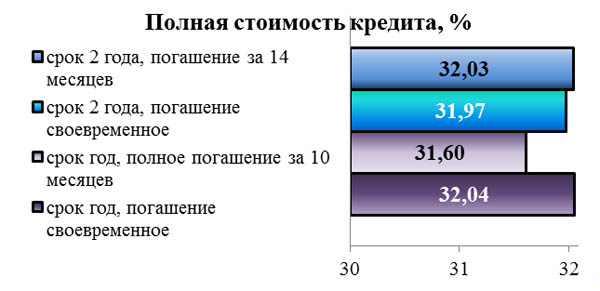

Does the term of the loan and early repayment affect the calculation

To answer the question, let's compare a loan in the amount of 120,000 at a rate of 28% for a period of 1 and 2 years.

For a loan with a term of one year, the TIC turned out to be 32.04%, with an increase in the term by 2 times, the value will decrease to 31.97%. These values are shown in white in the figure.

With an increase in the term, there is a decrease in the total cost, although it is insignificant.

Now let's determine the impact of early repayment on the size of the TIC. For a loan with a term of 1 year, we plan to repay the balance of the debt (principal debt) ahead of schedule along with the 10th installment.

For a loan for a period of 2 years - together with the 14th.

The figure shows that the change in the UCS is ambiguous. With a loan term of 2 years, early repayment increases the TIC, with a term of one year - reduces.

A case from one's life

Maxim: “There was such a problem - there was a mortgage. Initially, the contract indicated PSK 14.3%. After each early repayment, the schedule was recalculated. They gave a new value of PSK. As a result, after the second early payment, the total cost increased to 16.4%??? What this is connected with is not clear. Wrote a complaint. They gave an answer, but there is something unintelligible with reference to some formulas, calculations, etc.”

The complexity of calculation and interpretation makes the indicator inconvenient for personal use.

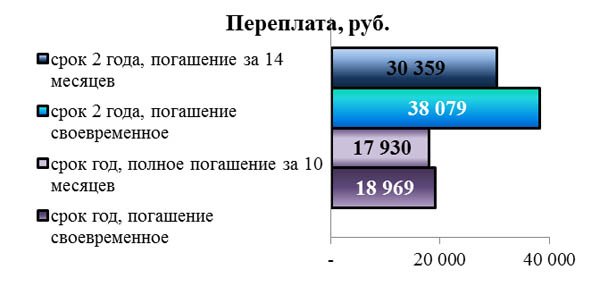

Let's compare the same options by the size of the overpayment.

For a loan for a period of 2 years, the borrower will overpay the bank 38,079 rubles, which is much more than for a year - 18,969. Early repayment definitely reduces the overpayment, regardless of the loan term. The indicator is clear. Therefore, in the case of early repayment, it is better to focus on the final overpayment, and not on the TIC indicator.

Again, let's refer to the amendments to the law. In accordance with what, banks will additionally calculate and bring to the borrower the TIC in monetary terms. It corresponds to the overpayment (if you do not delve into the question of its composition, taking into account commissions and insurances).

Does the method of calculation affect the UCS?

Annuity and differentiated payments.

Payments to repay a loan can be annuity (the same) and differentiated (decreasing due to a decrease in the amount of interest).

Let's do the calculation for the same example.

| Index | date | Differentiated payments | Annuity payments |

| approval date | 10.Jan.18 | -120 000,00 | -120 000,00 |

| payment 1 | Feb 10, 18 | 12 853,70 | 11 580,72 |

| payment 2 | 10.mar.18 | 12 362,74 | 11 580,72 |

| payment 3 | 10.apr.18 | 12 378,08 | 11 580,72 |

| payment 4 | May 10, 18 | 12 071,23 | 11 580,72 |

| payment 5 | 10.jun.18 | 11 902,47 | 11 580,72 |

| payment 6 | 10.Jul.18 | 11 610,96 | 11 580,72 |

| payment 7 | 10.Aug.18 | 11 426,85 | 11 580,72 |

| payment 8 | 10.Sep.18 | 11 189,04 | 11 580,72 |

| payment 9 | 10.oct.18 | 10 920,55 | 11 580,72 |

| payment 10 | 10.Nov.18 | 10 713,42 | 11 580,72 |

| payment 11 | 10.dec.18 | 10 460,27 | 11 580,72 |

| payment 12 | 10.Jan.19 | 10 237,81 | 11 580,72 |

| OVERPAID | 18 127,12 | 18 968,64 | |

| PSK | 0,3189 | 0,3204 | |

| PSK, % | 31,89 | 32,04 |

Differentiated payments are more profitable for the borrower. In them, the amount of the overpayment and the value of the TIC is less.

Accurate and approximate method of calculation.

With exact, the exact number of days in each month and year is taken into account. That is, in the month 30 or 31, and in February 28 or 29. In the year 365 or 366.

In an approximate way, each month consists of 30 days.

We will calculate the loan on the same terms with a differentiated payment.

| Index | date | Accurate payments | Approximate payments |

| approval date | 10.Jan.18 | -120 000,00 | -120 000,00 |

| payment 1 | Feb 10, 18 | 12 853,70 | 12 800,00 |

| payment 2 | 10.mar.18 | 12 362,74 | 12 566,67 |

| payment 3 | 10.apr.18 | 12 378,08 | 12 333,33 |

| payment 4 | May 10, 18 | 12 071,23 | 12 100,00 |

| payment 5 | 10.jun.18 | 11 902,47 | 11 866,67 |

| payment 6 | 10.Jul.18 | 11 610,96 | 11 633,33 |

| payment 7 | 10.Aug.18 | 11 426,85 | 11 400,00 |

| payment 8 | 10.Sep.18 | 11 189,04 | 11 166,67 |

| payment 9 | 10.oct.18 | 10 920,55 | 10 933,33 |

| payment 10 | 10.Nov.18 | 10 713,42 | 10 700,00 |

| payment 11 | 10.dec.18 | 10 460,27 | 10 466,67 |

| payment 12 | 10.Jan.19 | 10 237,81 | 10 233,33 |

| OVERPAID | 18 127,12 | 18 200,00 | |

| PSK | 0,3189 | 0,3205 | |

| PSK, % | 31,89 | 32,05 |

The exact method gave a lower value of overpayment and PSK.

Total cost calculation example

Full cost of consumer credit

Why is the total cost of the loan different from the interest rate?

The value of the TIC differs from the interest on the loan for two reasons:

1 TIC calculation takes into account not only interest payments. In these cases, the TIC value will always be higher than the interest rate.

2 The annual interest rate and TIC are mathematically different indicators. The value of TFR corresponds to the internal rate of return (IRR).

IRR characterizes the average annual yield of a loan for a bank or cost for a borrower. The formula is based on discounting and takes into account that the money you pay the bank "today" is worth more than the money paid at the end of the loan term.

Therefore, in most cases, even when taking into account only interest payments, TIC is higher than the interest rate.

Conclusion

The full cost is an informational indicator for choosing the optimal loan by the borrower.

Banks consider TIC as a percentage. As part of the PSK, they take into account insurance and other payments in different ways. The calculation is complex and ambiguous. It does not always allow you to correctly compare different options.

Therefore, the full cost must be considered by yourself, including all expected payments in the calculation. This will allow you to realistically evaluate each loan offer.

You can calculate the cost in the EXEL program or using one of the many loan calculators. It is important to calculate all options in one way (on only one calculator), because different calculators give different results.

If you are new to financial mathematics, it is better to focus on another indicator. Decide how much money you want to borrow and how long you really expect to repay. Calculate the amount of overpayment for different options. Pick the one that pays the least.

Dessert Video: Harley-Davidson Jumping